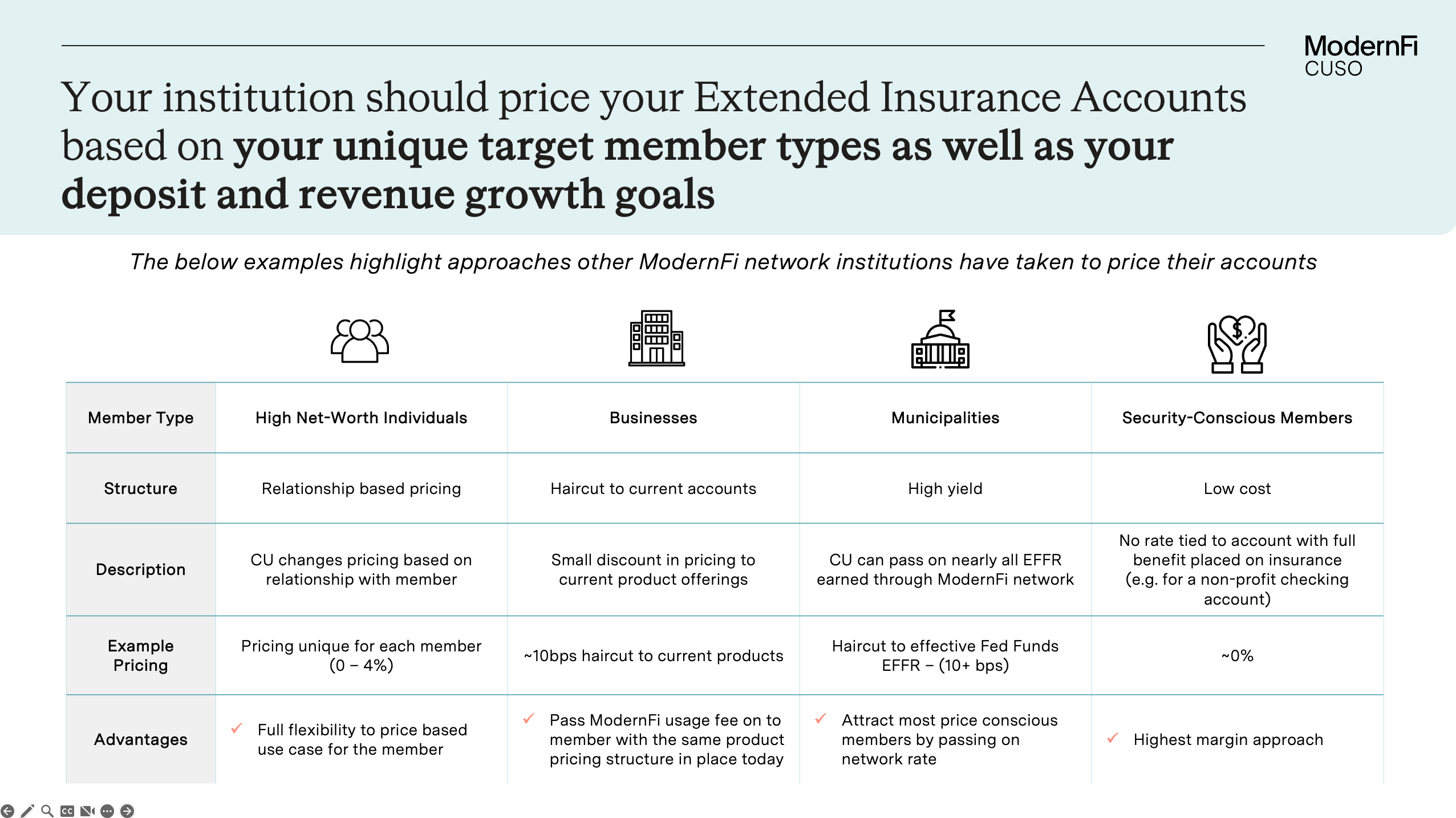

Pricing Structures

Funds swept into the ModernFi Network today generally yield Effective Federal Funds Rate (EFFR). You can choose to pass as much or as little of this yield as you would like on to your end members. Since these are overnight funds with no duration or term, you can respond quickly to interest rate changes by adjusting the interest rate offered on each of the Extended Insurance Accounts through your Admin Portal. ModernFi’s Admin Portal allows you to set individual interest rates for each of your Extended Insurance Accounts. This enables a few approaches to pricing structures:

- Flat Rate: You can establish a set rate for all Extended Insurance Accounts.

- Relationship-level Pricing: You can set Extended Insurance Account rates on an ad hoc basis, empowering your business services team to offer bespoke pricing for particularly high-value accounts. This could help you be competitive in winning significant funds and relationships.

- Tiered Pricing: Offer higher interest rates as account balances increase. This means the more funds a client maintains in their account, the better their rate, rewarding members for larger deposits and encouraging higher balances.

- Variable & Floating Rate: Link account rates to a recognized benchmark, such as the Federal Funds Rate (ex. Fed Funds - 1.00%). The interest rate will adjust periodically based on market conditions, ensuring your members always receive a competitive and up-to-date rate.

For ease of program management and unified marketing messaging, ModernFi recommends starting with a Flat Rate and/or Relationship-level Pricing. Below are some sample scenarios to help with your decision-making process.

Flat Rate – Discount to the Money Market: A credit union currently offers a 0.40% APY Money Market Account today for members with over $250,000 in deposits in their account. This credit union can price the Extended Insurance Account at a slight discount to the Money Market Account (i.e. 0.30%, a 10 bps discount to 0.40% the current Money Market Account). The credit union can dial this rate up or down as needed to achieve their Extended Insurance Account member growth goals. It’s important to note that the 0.30% rate is illustrative and provided as an example of how a flat rate could be set for all members.

Relationship-level Pricing – At the CU’s discretion: The credit union can use the Extended Insurance Account as a member retention and acquisition tool for extremely large value accounts (i.e. winning RFP, large business

accounts). The credit union can offer bespoke pricing to these particularly large accounts based on the amount of business they are willing to bring over on an aggregate basis (i.e. deposits, cash management services, business lending, merchant etc). You may choose to give your broad user base 0.30% while negotiating bespoke rates for larger accounts.

Updated 4 months ago